Venezuela Turns to Its Secretive Bag of Tricks to Avoid Default

by- One analyst sees $15.5 billion in assets on top of reserves

- Another says investors can’t count on any off-budget assets

Why Venezuela's Many Crises Keep Getting Worse

In the wake of Goldman Sachs’s controversial purchase of $2.8 billion of bonds held in Venezuela’s vaults, investors have been trying to quickly figure out what other hidden assets the country might be sitting on.

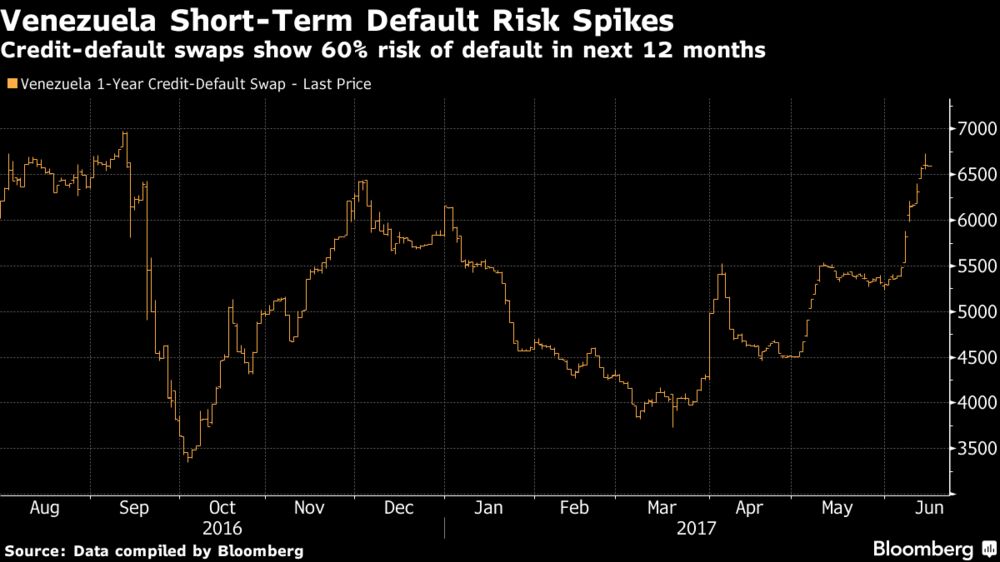

The stakes are high. As the central bank’s officially published foreign-reserve figure dwindles to just over $10 billion, that secretive stockpile might ultimately decide whether the nation averts default or not.

Calculating the value of those securities, as you might expect, is tricky. Estimates range from $15.5 billion of assets that could be made liquid from perennial contrarian Francisco Rodriguez to as little as zero from Nomura Inc.’s Siobhan Morden. Barclays Plc landed in the middle, at about $10 billion.

Adding to the complex calculations is speculation that Venezuela is going to have a tougher and tougher time finding buyers for these securities. After Goldman was loudly criticized in Venezuela and abroad for last month’s deal, Wall Street banks and investors are growing increasingly hesitant to finance a regime that’s routinely accused of human-rights violations and blamed for widespread shortages of food, medicine and other basic necessities.

“There’s something that has undergone a big change,” said Alejandro Grisanti, the director of the Caracas-based consultancy Ecoanalitica. “And that’s the issue of the market’s willingness to buy what has been offered.”

Reserves & Gold

Venezuela reports foreign reserves of about $10.4 billion, $7.6 billion of which is composed of gold that was on the central bank’s balance sheet as of March. The cash component is easy enough to spend, but questions have swirled around the gold since ex-president Hugo Chavez brought most of it into the country several years ago. It’s unclear how much is still in Caracas and how much has been sent back to overseas banks where it could be counted as collateral to raise funds. (Officials at the Finance Ministry declined to comment, while the central bank didn’t return emails seeking comment. Venezuela President Nicolas Maduro, for his part, has promised he has the funds to pay debt through next year.)

Wherever Venezuela’s gold is, it isn’t particularly easy to sell billions of dollars of precious metal. That’s why Grisanti, a former head of Latin America research at Barclays, doubts that the reserves should be considered truly liquid.

Bonds

Then there’s the murkier set of assets. Some of the bond stash is believed to date from a highly unusual practice that the government had for pumping dollars into the foreign-exchange market through the Venezuelan central bank. Others may have been purchased by government entities including pension funds. It’s been tough for investors to get a handle on how much of the bonds are still knocking around in Venezuela.

One big chunk surfaced last month when Goldman Sachs purchased $2.8 billion of securities that had previously been held by the central bank. Goldman bought the bonds at a deep discount, triggering outrage among Venezuela’s critics, who accused the bank of throwing a lifeline to Maduro. There’s still $5 billion of sovereign bonds due 2036 that were sold to a state bank. Traders have said they’ve seen attempts to shop those around too.

In all, Barclays analyst Alejandro Arreaza estimates Venezuela could raise up to $4.4 billion selling the securities. Rodriguez, the chief economist at Torino Capital, estimates the government could squeeze $5.1 billion out of them, especially if it seizes onshore bonds held by locals.

Cash Accounts

Venezuela also has funds in various off-balance-sheet accounts. Barclays estimates it’s as much as $6.1 billion, though how much of that is truly accessible is unclear because some portion comes from Chinese loans that carry restrictions on their use.

Rodriguez counts $4.8 billion in off-budget funds. He also puts a value on trade credits associated with Venezuela’s program of selling cheap oil to allies in the Caribbean and Central America. He says Venezuela may be able to monitize the IOUs to the tune of $3.5 billion. He also thinks the country could raise another $2 billion by selling various public-sector overseas investments.

“Most of these assets are illiquid,” Rodriguez said. “They can be sold, or securitized, and so they can be made liquid.”

The next big test for how long the money will last is October, when the state oil company has to make a payment of just under $1 billion on its 2020 bond.

Keine Kommentare:

Kommentar veröffentlichen