Venezuela hat viel Öl - aber kaum noch Geld: Nun hat Präsident Maduro eigenmächtig eine "Neuordnung" der Verbindlichkeiten angeordnet - und könnte eine neue Finanzkrise in Südamerika auslösen.

Das krisengeschüttelte Venezuela hat eine Neuordnung seiner Auslandsschulden angekündigt - und riskiert damit womöglich eine Staatspleite. Präsident Nicolas Maduro verkündete, er habe eine Refinanzierung und Umstrukturierung der ausländischen Verbindlichkeiten angeordnet. Es gehe darum, den Bedürfnissen der unter Versorgungsengpässen leidenden Bevölkerung gerecht zu werden.

Wie er sich das konkret vorstellt, sagte Maduro nicht. Unter Verweis auf die US-Sanktionen sprach er von einem "Kampf gegen die finanzielle Schikanierung" des Landes. Zuvor werde Venezuela eine noch diese Woche fällig werdende Anleihe-Zahlung des staatlichen Ölkonzerns PDVSA über 1,1 Milliarden Dollar leisten.

Venezuelas Schulden werden auf 150 Milliarden Dollar geschätzt - und übersteigen damit die Devisenreserven des Landes in Höhe von zehn Milliarden Dollar deutlich. Im Juli hatte die US-Ratingagentur Standard & Poor's (S&P) die ohnehin schon schwache Bonität Venezuelas weiter heruntergestuft und von einem negativen Ausblick gesprochen. Was macht Russland?

Größte Gläubiger des Landes sind China mit 23 Milliarden an Forderungen und Russland mit acht Milliarden. Die USA haben Venezuela mit Sanktionen belegt. US-Präsident Donald Trump untersagte per Dekret den Handel mit neuen venezolanischen Staatsanleihen. Betroffen ist auch PDVSA, der eine wichtige Einnahmequelle für Venezuela darstellt. Ölverkäufe bilden das Fundament der venezolanischen Wirtschaft und stehen für 95 Prozent der Exporte. Doch die Einnahmen sind zuletzt wegen fallender Erdölpreise deutlich zurückgegangen.

Maduro plans one more payment on PDVSA bonds maturing Nov. 2

From there on out, the nation will try to renegotiate its debt

Venezuelan President Nicolas MaduroPhotographer: Wil Riera/Bloomberg

President Nicolas Maduro said Venezuela will seek to restructure its global debt after the state oil company makes one more payment, blaming U.S. sanctions for making it impossible to find new financing.

The government will transfer funds for a $1.1 billion principal payment on Petroleos de Venezuela bonds that came due Thursday, Maduro said from Caracas. From there on out, the nation will renegotiate its debt with banks and investors, he said in a national address.

It’s a step that Maduro and his late predecessor, Hugo Chavez, rejected for two decades -- defying Wall Street analysts in recent years as cash drained from the government’s coffers, and making the nation’s debt one of the more profitable trades in emerging markets. By seeking a restructuring, Maduro is acknowledging that the heavy debt load for the oil exporting nation has become unsustainable amid a drop in crude output and prices, as well as the financial sanctions. He didn’t say if the country will make other debt payments that are coming due in the next weeks, creating a degree of confusion among investors.

It’s “going to be ugly for holders,” said Ray Zucaro, the chief investment officer at Miami-based RVX Asset Management, which holds the PDVSA bonds that matured Thursday. “There’s no real way to sugar coat.”

Venezuelan bonds trade at an average price of 36 cents on the dollar, reflecting widespread investor concern that the nation was headed for default. While notes due in 2027 have plunged from about 50 cents on the dollar a year ago to 38.7 on Thursday, securities maturing next year have been trading at about 65 cents.

Even after the oil producer known as PDVSA made an $842 million principal payment Oct. 27, the nation is behind on about $800 million of interest payments. All told, there’s $143 billion in foreign debt owed by the government and state entities, with about $52 billion in bonds, according to Torino Capital.

Sanctions imposed in August by the U.S. have made it difficult to raise money from international investors, and effectively prohibit refinancing or restructuring existing debt, because they block U.S.-regulated institutions from buying new bonds. It’s an unprecedented situation for bondholders, who have limited recourse as long as sanctions are in effect.

“I decree a refinancing and restructuring of external debt and all Venezuelan payments,” Maduro said. “We’re going to a complete reformatting. To find an equilibrium, and to cover the necessities of the country, the investments of the country.”

Vice President Tareck El Aissami, one of the individuals targeted in the sanctions, was named head of bond restructuring efforts. Earlier this year, the Treasury Department alleged that El Aissami -- who was elevated to his post in January -- protected drug lords and oversaw a network exporting thousands of kilograms of cocaine.

The U.S. has accused the Maduro government of human-rights violations, and President Donald Trump called the turmoil there -- with more than 100 lives lost in street protests earlier this year -- “a disgrace to humanity.” The regime’s sweeping victories in October’s gubernatorial elections have been marred by fraud accusations.

Maduro made the announcement in a televised address in which he emphasized that Venezuela has always honored its obligations, and had the money to continue doing so, but was being hampered by the financial penalties the U.S. imposed.

Throughout the broadcast, Maduro kept Wall Street viewers on the edge of their seats by teasing an upcoming “historic announcement on debt,” then spending a half hour touting new ambulances and public roads as he waited for the international media to tune in.

His announcement left viewers confused as to why the government would opt to restructure after making two large bond payments, money that presumably could have been used to buy medications and other supplies in shortage. Some analysts even raised the idea that perhaps Maduro was confused about bond terminology and didn’t mean to say that he plans on restructuring the debt. Others speculated he plans on excluding PDVSA from the process.

“It makes no sense defaulting while paying tomorrow,” said economist Asdrubal Oliveros, the director of the Caracas consultancy Ecoanalitica.

Attorneys and investors say a restructuring of all Venezuelan debt would be enormously complicated, even if sanctions are lifted at some point. Creditors will have to figure out a sustainable repayment plan for the government and possibly PDVSA. Fights between creditors will be inevitable as they sort out who’s entitled to what. In addition to all the bonds, Venezuela owes billions of dollars in awards resulting from international arbitration disputes and to private companies with cash trapped in the country, while PDVSA and its subsidiaries have a slew of outstanding loans.

“This promises to be as complex a restructuring exercise as I’ve seen in my more than 30 years of experience in this market,” said Hans Humes, the chief executive officer of emerging-markets hedge fund Greylock Capital Management.

The Institute of International Finance will hold a call for creditors Friday to discuss Maduro’s plan, according to an email to investors seen by Bloomberg.

There are plenty of Venezuela watchers -- including economists such as Ricardo Hausmann -- who have been urging the government to stop payments on its bonds and to seek aid from lenders like the International Monetary Fund. They say the debt load is unsustainable, and sending dollars to foreign investors while cutting back on imports of food, medicine and basic goods for the Venezuelan people is immoral.

Venezuela’s decision to stay current on its debt has confounded socialists and capitalists alike, but it probably boils down to the risk that Venezuela’s international oil assets could get seized by creditors or tied up in court.

Through PDVSA, Venezuela -- home to the world’s largest petroleum reserves -- has offshore refineries and oil receivables. PDVSA’s U.S. refining arm, Citgo Holding Inc., has also been used as collateral to back some bonds. And if creditors start going after Venezuela’s oil assets, buyers of its crude are apt to turn to other sources, depressing not only demand but the price of Venezuela’s main treasure.

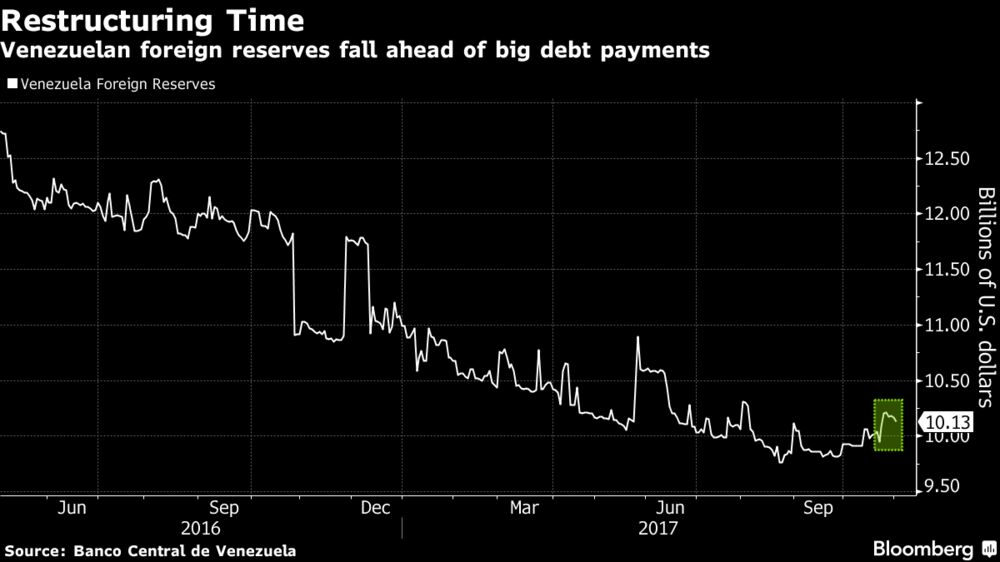

Thanks to Maduro’s gross mismanagement, Venezuela is suffering one of the worst economic collapses in modern Latin American history. Its economy contracted 19 percent last year, according to its central bank, while the IMF expects annual inflation to hit more than 2,000 percent next year. A socialist revolution that came to power in 1999 vowing to raise up the forgotten poor and bring down the corrupt elite has driven the poverty rate to 82 percent of the population and has itself looted billions of dollars. International reserves have sunk to a 15-year low near $10 billion.

After surviving a coup in 2002, former president Chavez imposed currency controls limiting the amount of dollars that individuals could buy or what companies could purchase for imports. As the black market exchange rate widened from the official rate, he eventually began to use bond sales as a means to alleviate the demand for hard currency and mop up excess liquidity in bolivars. He achieved that by selling dollar-denominated notes to locals in bolivars. They then sold them abroad to foreign investors.

“The one who created this monster of debt is the government, during the time of the highest oil income ever,” said Julio Borges, the president of the opposition-led National Assembly.

Even with oil revenue pouring in at a record clip, Chavez began to sign long-term lending programs with China. The deals consisted of China delivering billions in cash for infrastructure and social programs while Venezuela pledged future oil deliveries.

While the short-term influx of money helped Chavez bankroll various projects, over time the strain of exporting hundreds of thousands of barrels to pay back the loans took its toll. In addition, investment in exploration and production has dried up after prices tanked and output is currently below 2 million barrels a day, down by more than a third in the past 15 years.

Because Venezuela isn’t current with most of its key economic statistics, the most basic data an investor would use to gauge the country’s creditworthiness haven’t been made available. Still, credit default swap traders placed the implied probability of a Venezuelan default at 97 percent over the next five years.

“There’s a bad scenario, which has essentially happened now, in which the regime defaults, there’s no change in regime and with the sanctions there’s no restructuring,” Gorky Urquieta, who helps manage $15 billion in emerging-market debt at Neuberger Berman, said by phone from Atlanta. “The whole idea of recovery value takes on a whole new meaning, and there’s not much bondholders will be able to do.”

— With assistance by Andrew Rosati, Jose Enrique Arrioja, and Daniela Guzman

#BUSINESS NEWSNOVEMBER 1, 2017 / 10:08 PM / UPDATED 8 HOURS AGO Some bondholders have received late PDVSA bond payment: sources

Reuters Staff

2 MIN READ

CARACAS (Reuters) - Some bondholders have received a payment on Venezuelan state oil company PDVSA’s 2020 bond that came due last week, three market sources said on Wednesday, allaying earlier concerns over the delay.

FILE PHOTO: The corporate logo of the state oil company PDVSA is seen at a gas station in Caracas, Venezuela, August 30, 2017. REUTERS/Andres Martinez Casares/File Photo

The focus for investors now switches to a $1.2 billion payment on a different bond due on Thursday.

The 2020 bond payment delay came at a time of worries that PDVSA will struggle to service debt due to an economic crisis spurred by the collapse of Venezuela’s socialist economic model.

President Nicolas Maduro insists the country and PDVSA will honor all debts and says default talk is a campaign against his government.

The $842 million amortization payment on the PDVSA 2020 716558AH4= bond was due last Friday.

But bondholders for several days said they had not received the funds, and complained of confusion over which financial services institutions were in charge of making transfers.

“Yes, they paid,” said an executive of a fund that invests in Venezuelan bonds.

PDVSA did not immediately respond to an email seeking comment.

On Thursday, the company faces a $1.2 billion principal and interest payment on its maturing 2017N bond VE055409692=.

Venezuela and PDVSA bonds were up across the board on Wednesday, following reports that the 2020 bond payment would be delivered by Thursday.

Reporting by Corina Pons, writing by Brian Ellsworth, editing by Rosalba O'Brien

Our Standards:The Thomson Reuters Trust Principles.

what a joke...the country is as bankrupt as every but they will find buyers for the bonds.. i am sure.

***The Greek government is planning an unprecedented debt swap worth 29.7 billion euros ($34.5 billion) aimed at boosting the liquidity of its paper and easing the sale of new bonds in the future.

Under a project that could be launched in mid November, the government plans to swap 20 bonds issued after a restructuring of Greek debt held by private investors in 2012 with as many as five new fixed-coupon bonds, according to two senior bankers with knowledge of the swap plan. The bank officials requested anonymity as the plan has yet to be made public. The maturities of the new bonds may be the same as for the existing notes, which range from 2023 to 2042.

“The move aims to address the current illiquidity of the Greek bond market,” according to analysts at Pantelakis Securities SA in Athens. It will also “establish a decent yield curve, thus facilitating the country’s return to public debt markets.”

The move comes as Greece prepares for life after the end of its current bailout program in August 2018. The debt swap is a step toward the country’s full return to markets required to avoid a new bailout program. The government plans to tap the bond market in 2018 to raise at least 6 billion euros to create an adequate buffer to honor debt obligations, according to a government official.***

#AFRICATECHOCTOBER 31, 2017 / 9:03 PM / UPDATED 3 HOURS AGO

UPDATE 4-Venezuela PDVSA bondholders to receive late payment by Thursday -sources

Reuters Staff

3 MIN READ

(Adds Euroclear declining to comment, paragraph 5)

By Corina Pons and Brian Ellsworth

CARACAS, Oct 31 (Reuters) - Holders of one of Venezuelan state oil company PDVSA’s distressed bonds will by Thursday receive an amortization payment that was due last week, according to a message from U.S. trust company DTC seen by five market sources on Tuesday.

The news confirmed that the crisis-stricken nation is continuing to prioritize debt service payments despite an unraveling socialist economy that is suffering triple-digit inflation and Soviet-style product shortages.

And it boded well for the $1.2 billion interest and principal payment on PDVSA’s 2017N bond that matures on Thursday but signaled that unexplained delays are likely to persist.

“DTC transferred to Euroclear at 3 p.m. ... Clients will see it in their accounts on Thurs morning,” said a message sent by DTC, according to market sources. DTC is officially called Depository Trust Company, and the message referred to settlement agent Euroclear.

Both DTC and Euroclear declined to comment.

Bondholders had since Friday been unable to figure out where the $842 million amortization payment on the PDVSA 2020 bond had ended up. PDVSA on Friday said it had transferred the funds, but the money had not appeared investors’ accounts.

Many had described confusion over which financial institutions were in charge of transferring the funds to bondholders. Silence from PDVSA and the officially designated intermediaries fueled market nervousness.

PDVSA did not immediately respond to an email seeking comment.

The company’s bonds were little changed on the news, having slipped slightly on Tuesday as the market largely shrugged off concerns about the delay, according to Thomson Reuters data.

PDVSA’s 2017N bond maturing on Thursday was down 0.125 percentage points to a bid price of 95.375, while PDVSA’s 2022 bond was down 0.740 percentage points to bid 45.510.

President Nicolas Maduro says the country is the victim of an “economic war” led by his political adversaries and exacerbated by recent economic sanctions by the government of U.S. President Donald Trump.

His critics insist that years of squandering oil revenue and dysfunctional price and currency controls have steadily unwound the economy, leaving millions unable to eat properly.

Maduro insists that the government will honor all of its debt commitments and describes default talk as a smear campaign against the ruling socialists.

Since early October PDVSA and Venezuela have been delaying the payment of bond coupons, using a 30-day grace period to push payments down the road. They now have close to $750 million in unpaid coupons that come due within the next month.

Separately, Venezuela made a late payment of $74 million to holders of securities called Oil-Indexed Payment Obligations, which were originally issued in 1990, Bank of New York Mellon said in a newspaper advertisement on Tuesday. (Reporting by Brian Ellsworth and Corina Pons; Editing by Susan Thomas and Cynthia Osterman)

Venezuela PDVSA bondholders to receive late payment by Thursday: sources

Corina Pons, Brian Ellsworth

3 MIN READ

CARACAS (Reuters) - Holders of one of Venezuelan state oil company PDVSA’s distressed bonds will by Thursday receive an amortization payment that was due last week, according to a message from U.S. trust company DTC seen by five market sources on Tuesday.

FILE PHOTO: The corporate logo of the state oil company PDVSA is seen at a gas station in Caracas, Venezuela, August 30, 2017. REUTERS/Andres Martinez Casares/File Photo

The news confirmed that the crisis-stricken nation is continuing to prioritize debt service payments despite an unraveling socialist economy that is suffering triple-digit inflation and Soviet-style product shortages.

And it boded well for the $1.2 billion interest and principal payment on PDVSA’s 2017N bond that matures on Thursday but signaled that unexplained delays are likely to persist.

“DTC transferred to Euroclear at 3 p.m. ... Clients will see it in their accounts on Thurs morning,” said a message sent by DTC, according to market sources. DTC is officially called Depository Trust Company, and the message referred to settlement agent Euroclear.

DTC declined to comment on the message. A Euroclear spokesman did not immediately respond to request for comment.

Bondholders had since Friday been unable to figure out where the $842 million amortization payment on the PDVSA 2020 bond had ended up. PDVSA on Friday said it had transferred the funds, but the money had not appeared investors’ accounts.

Many had described confusion over which financial institutions were in charge of transferring the funds to bondholders. Silence from PDVSA and the officially designated intermediaries fueled market nervousness.

PDVSA did not immediately respond to an email seeking comment.

The company’s bonds were little changed on the news, having slipped slightly on Tuesday as the market largely shrugged off concerns about the delay, according to Thomson Reuters data.

PDVSA’s 2017N bond VE055409692= maturing on Thursday was down 0.125 percentage points to a bid price of 95.375, while PDVSA’s 2022 bond VE059352415= was down 0.740 percentage points to bid 45.510.

President Nicolas Maduro says the country is the victim of an “economic war” led by his political adversaries and exacerbated by recent economic sanctions by the government of U.S. President Donald Trump.

His critics insist that years of squandering oil revenue and dysfunctional price and currency controls have steadily unwound the economy, leaving millions unable to eat properly.

Maduro insists that the government will honor all of its debt commitments and describes default talk as a smear campaign against the ruling socialists.

Since early October PDVSA and Venezuela have been delaying the payment of bond coupons, using a 30-day grace period to push payments down the road. They now have close to $750 million in unpaid coupons that come due within the next month.

Separately, Venezuela made a late payment of $74 million to holders of securities called Oil-Indexed Payment Obligations, which were originally issued in 1990, Bank of New York Mellon said in a newspaper advertisement on Tuesday.