Venezuela Will Seek to Restructure Its Debt

By , , , and

Updated on

- Maduro plans one more payment on PDVSA bonds maturing Nov. 2

- From there on out, the nation will try to renegotiate its debt

President Nicolas Maduro said Venezuela will seek to restructure its global debt after the state oil company makes one more payment, blaming U.S. sanctions for making it impossible to find new financing.

The government will transfer funds for a $1.1 billion principal payment on Petroleos de Venezuela bonds that came due Thursday, Maduro said from Caracas. From there on out, the nation will renegotiate its debt with banks and investors, he said in a national address.

It’s a step that Maduro and his late predecessor, Hugo Chavez, rejected for two decades -- defying Wall Street analysts in recent years as cash drained from the government’s coffers, and making the nation’s debt one of the more profitable trades in emerging markets. By seeking a restructuring, Maduro is acknowledging that the heavy debt load for the oil exporting nation has become unsustainable amid a drop in crude output and prices, as well as the financial sanctions. He didn’t say if the country will make other debt payments that are coming due in the next weeks, creating a degree of confusion among investors.

It’s “going to be ugly for holders,” said Ray Zucaro, the chief investment officer at Miami-based RVX Asset Management, which holds the PDVSA bonds that matured Thursday. “There’s no real way to sugar coat.”

Venezuelan bonds trade at an average price of 36 cents on the dollar, reflecting widespread investor concern that the nation was headed for default. While notes due in 2027 have plunged from about 50 cents on the dollar a year ago to 38.7 on Thursday, securities maturing next year have been trading at about 65 cents.

Even after the oil producer known as PDVSA made an $842 million principal payment Oct. 27, the nation is behind on about $800 million of interest payments. All told, there’s $143 billion in foreign debt owed by the government and state entities, with about $52 billion in bonds, according to Torino Capital.

Sanctions imposed in August by the U.S. have made it difficult to raise money from international investors, and effectively prohibit refinancing or restructuring existing debt, because they block U.S.-regulated institutions from buying new bonds. It’s an unprecedented situation for bondholders, who have limited recourse as long as sanctions are in effect.

“I decree a refinancing and restructuring of external debt and all Venezuelan payments,” Maduro said. “We’re going to a complete reformatting. To find an equilibrium, and to cover the necessities of the country, the investments of the country.”

Vice President Tareck El Aissami, one of the individuals targeted in the sanctions, was named head of bond restructuring efforts. Earlier this year, the Treasury Department alleged that El Aissami -- who was elevated to his post in January -- protected drug lords and oversaw a network exporting thousands of kilograms of cocaine.

The U.S. has accused the Maduro government of human-rights violations, and President Donald Trump called the turmoil there -- with more than 100 lives lost in street protests earlier this year -- “a disgrace to humanity.” The regime’s sweeping victories in October’s gubernatorial elections have been marred by fraud accusations.

Maduro made the announcement in a televised address in which he emphasized that Venezuela has always honored its obligations, and had the money to continue doing so, but was being hampered by the financial penalties the U.S. imposed.

Throughout the broadcast, Maduro kept Wall Street viewers on the edge of their seats by teasing an upcoming “historic announcement on debt,” then spending a half hour touting new ambulances and public roads as he waited for the international media to tune in.

His announcement left viewers confused as to why the government would opt to restructure after making two large bond payments, money that presumably could have been used to buy medications and other supplies in shortage. Some analysts even raised the idea that perhaps Maduro was confused about bond terminology and didn’t mean to say that he plans on restructuring the debt. Others speculated he plans on excluding PDVSA from the process.

“It makes no sense defaulting while paying tomorrow,” said economist Asdrubal Oliveros, the director of the Caracas consultancy Ecoanalitica.

Attorneys and investors say a restructuring of all Venezuelan debt would be enormously complicated, even if sanctions are lifted at some point. Creditors will have to figure out a sustainable repayment plan for the government and possibly PDVSA. Fights between creditors will be inevitable as they sort out who’s entitled to what. In addition to all the bonds, Venezuela owes billions of dollars in awards resulting from international arbitration disputes and to private companies with cash trapped in the country, while PDVSA and its subsidiaries have a slew of outstanding loans.

“This promises to be as complex a restructuring exercise as I’ve seen in my more than 30 years of experience in this market,” said Hans Humes, the chief executive officer of emerging-markets hedge fund Greylock Capital Management.

The Institute of International Finance will hold a call for creditors Friday to discuss Maduro’s plan, according to an email to investors seen by Bloomberg.

There are plenty of Venezuela watchers -- including economists such as Ricardo Hausmann -- who have been urging the government to stop payments on its bonds and to seek aid from lenders like the International Monetary Fund. They say the debt load is unsustainable, and sending dollars to foreign investors while cutting back on imports of food, medicine and basic goods for the Venezuelan people is immoral.

Venezuela’s decision to stay current on its debt has confounded socialists and capitalists alike, but it probably boils down to the risk that Venezuela’s international oil assets could get seized by creditors or tied up in court.

Through PDVSA, Venezuela -- home to the world’s largest petroleum reserves -- has offshore refineries and oil receivables. PDVSA’s U.S. refining arm, Citgo Holding Inc., has also been used as collateral to back some bonds. And if creditors start going after Venezuela’s oil assets, buyers of its crude are apt to turn to other sources, depressing not only demand but the price of Venezuela’s main treasure.

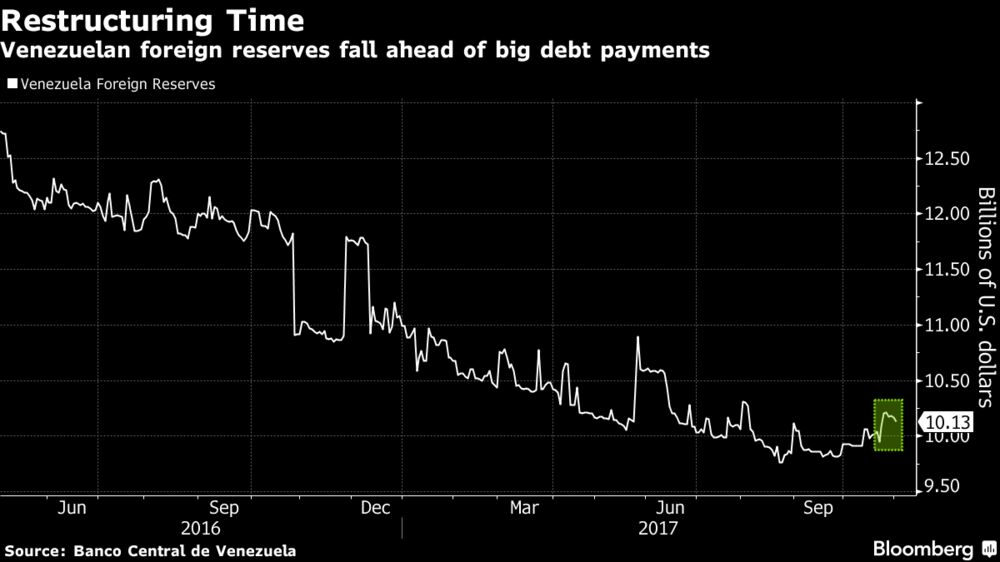

Thanks to Maduro’s gross mismanagement, Venezuela is suffering one of the worst economic collapses in modern Latin American history. Its economy contracted 19 percent last year, according to its central bank, while the IMF expects annual inflation to hit more than 2,000 percent next year. A socialist revolution that came to power in 1999 vowing to raise up the forgotten poor and bring down the corrupt elite has driven the poverty rate to 82 percent of the population and has itself looted billions of dollars. International reserves have sunk to a 15-year low near $10 billion.

After surviving a coup in 2002, former president Chavez imposed currency controls limiting the amount of dollars that individuals could buy or what companies could purchase for imports. As the black market exchange rate widened from the official rate, he eventually began to use bond sales as a means to alleviate the demand for hard currency and mop up excess liquidity in bolivars. He achieved that by selling dollar-denominated notes to locals in bolivars. They then sold them abroad to foreign investors.

“The one who created this monster of debt is the government, during the time of the highest oil income ever,” said Julio Borges, the president of the opposition-led National Assembly.

Even with oil revenue pouring in at a record clip, Chavez began to sign long-term lending programs with China. The deals consisted of China delivering billions in cash for infrastructure and social programs while Venezuela pledged future oil deliveries.

While the short-term influx of money helped Chavez bankroll various projects, over time the strain of exporting hundreds of thousands of barrels to pay back the loans took its toll. In addition, investment in exploration and production has dried up after prices tanked and output is currently below 2 million barrels a day, down by more than a third in the past 15 years.

Because Venezuela isn’t current with most of its key economic statistics, the most basic data an investor would use to gauge the country’s creditworthiness haven’t been made available. Still, credit default swap traders placed the implied probability of a Venezuelan default at 97 percent over the next five years.

“There’s a bad scenario, which has essentially happened now, in which the regime defaults, there’s no change in regime and with the sanctions there’s no restructuring,” Gorky Urquieta, who helps manage $15 billion in emerging-market debt at Neuberger Berman, said by phone from Atlanta. “The whole idea of recovery value takes on a whole new meaning, and there’s not much bondholders will be able to do.”

— With assistance by Andrew Rosati, Jose Enrique Arrioja, and Daniela Guzman

Keine Kommentare:

Kommentar veröffentlichen