You won’t find a certain Latin phrase anywhere on it. Still, just for the record, here’s evidence that Argentina did learn at least one thing from the pari passu saga.

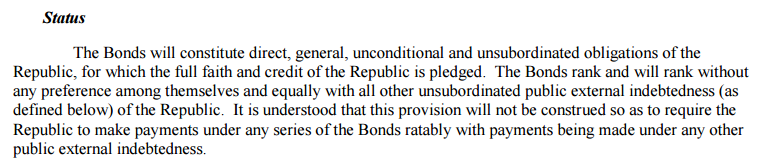

Presenting the new pari passu clause, from the prospectus for the gargantuan $16.5bn bond which Argentina is issuing to pay off holdouts and place that saga behind it:

Click to enlarge.

The entire prospectus runs to 266 pages incidentally, but this little tidbit has an interesting history.

For any of the investors proposing to lend to Argentina who will actually care to look — almost none will — it probably seems like any other sovereign promise to treat creditors equally. However, there has been a small but important rewriting. It disavows a promise to treat them ratably.

That means Argentina’s new clause will exorcise the old one attached to its pre-default debt. This didn’t rule out paying each creditor what they were owed in lockstep, a mistake which made the saga possible in the first place. It let US judges decide it was fair to impose an injunction on Argentina to pay its holdouts alongside everyone else for as long as it was “recalcitrant” about doing a deal.

That injunction was only just lifted in the nick of time last week to allow this bond issue to go ahead.

It also means the new terms will follow the International Capital Market Association’s template clause (issued last year) to stop future sagas afflicting sovereign debtors who restructure their bonds. Other governments are steadily including the clause in new debts, even governments whose creditors might spit fire at any reduction in their rights. Greece did it years ago. So did Ecuador.

Firstly, it’s a slight pity that it will cost Argentina over $8bn to correct its mistake.

Elliott and three other funds who together pioneered the pari passu lawsuits against Argentina will alone take a $4.65bn slice of that overall figure so far for holdout settlements, for example. It comes to about $53m per word of the new clause. It must be one of the most expensive editing jobs in history.

Which leads to an interesting question.

In this bond — of all bonds — why didn’t Argentina simply remove the clause altogether, just in case it goes wrong next time?

The new bond does much else to remove the threat of holdouts when if Argentina defaults on it in future. There are new-style collective action clauses to bind holdouts to a majority vote to accept restructuring terms. The right of individual creditors to sue is taken away, to instead lie with the bond trustee. This is increasingly common in sovereign debt. But there’s the possibility of direct amputation too.

As mentioned, no real-world bondholder is going to take the time to look for a pari passu clause, let alone decide whether they should refuse to lend to Argentina if one isn’t there. In a negative rates world 8 per cent yield talks rather louder.

And complete removal is something that the ICMA drafters considered when they were thinking how to redesign pari passu after Argentina’s saga.

Pari passu might have meant something clear long ago in sovereign debt, in an age when global finance wasn’t as powerful and sovereigns could happily pass laws to explicitly rank some creditors below others, with only those with gunboats to worry about. Argentina’s notorious lock law might have been a modern revival, but no government would surely be that stupid again.

As Lee Buchheit and Sofia Martos wrote two years ago, in the Journal of International Banking and Finance Law:

One obvious alternative is to remove the clause in its entirety. We now know that the danger the pari passu clause was originally designed to address – the risk of involuntary subordination – exists only in a very few countries. The clause serves no useful function in countries whose laws do not permit the involuntary subordination of an existing creditor, which is why it does not appear in the standard documentation for domestic debt issuances in most countries. So jettisoning the clause altogether will not adversely affect the position of creditors and will avoid the risk of further aberrant judicial interpretations down the road.

But they also pointed out the problem:

Never having had a clear idea of what purpose the pari passu clause actually served in a cross-border debt instrument, underwriters and most investors will surely not have a clear idea of the implications of not having it. The guiding principle of the underwriting community in matters of documentation has always been that if it was good enough for my father, it’s good enough for me. Excising the clause altogether could therefore entail a significant educational initiative.

And that may simply be the end of the story. The inertia of quite a lot of finance.

Argentina wants to issue this debt, and make its bond-market return, as quickly as possible. Investors are equally keen to grab a piece of a credit they have not seen grace the market without interruption for many years.

Sovereign pari passu is going back to what it used to be, a fuzzy memory, this time with the ratable payments disavowal added to it as an insurance policy.

Will it hold? Probably. Does it make it even more amazing that this whole saga happened in the first place? Just maybe.

Keine Kommentare:

Kommentar veröffentlichen