Venezuela's Descent Into World's Riskiest Sovereign Credit: Q&A

Venezuela is running out of money.

The price of oil, which makes up almost all of the country’s exports, has tumbled 75 percent in the past three years and investors are predicting the country is on course for the biggest-ever emerging-market sovereign default. No nation in the world is more likely to miss payments, according to traders of its credit-default swaps.

The country already tops measures of the world’s most miserableeconomy, with inflation of 181 percent last year, a currency that has collapsed on the black market to less than 1 percent of its official value and shortages of basic goods such as detergent and antibiotics. It’s a horrific turnaround for what was once one of the region’s most stable democracies, famous for its big cars, cheap gasoline and beauty queens.

While bond prices suggest that most investors are confident the country will make good on a $1.5 billion obligation coming due Feb. 26, and Venezuela appeared to take steps over the past few weeks to raise cash, the outlook dims for $4.1 billion of notes the state oil company is due to pay back in October and November.

Here are answers to some of the most frequently asked questions about Venezuela:

How much debt does Venezuela have?

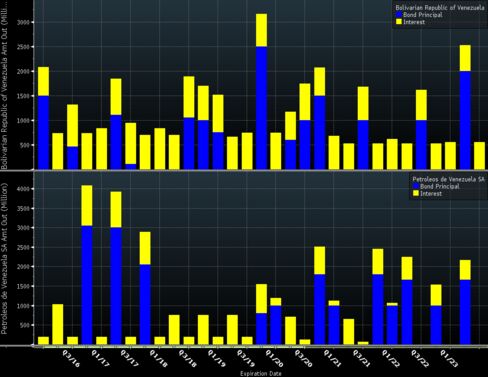

Venezuela has $35.6 billion of dollar bonds outstanding and owes $67 billion once interest payments are included. State-owned oil company Petroleos de Venezuela SA, known as PDVSA, has $33.5 billion of bonds, and $52.6 billion counting interest.

If there’s a default, when is it most likely to come?

Venezuela probably has the cash to pay back the bonds coming due in February along with $326 million of interest payments this month. In October and November of this year, PDVSA needs to pay back $4.1 billion of bonds and $1 billion in interest. The notes’ price of about 60 cents on the dollar indicate skepticism the country will be able to do that.

Trading in the credit-default swaps market suggests there’s a 70 percent chance Venezuela will default in the next 12 months.

What might the recovery value of the bonds be?

Estimates vary between 20 cents on the dollar and as much as 71 cents in the case of PDVSA bonds. Since Venezuela is so reliant on oil, the value is hugely dependent on the price of crude. Projections compiled by Bloomberg for the year-end price of West Texas Intermediate range between $30 and $70 a barrel.

A second factor is the exchange rate Venezuela uses. The government announced Feb. 17 that Venezuela would devalue the foreign-exchange rate used for priority imports by 36 percent to 10 bolivars per dollar. There’s another official rate of 202.9 per dollar for other transactions. That’s not to mention the black-market rate of more than 1,000 per dollar. A weaker currency would lower the ratio of debt to the size of the economy, improve the country’s trade balance, and reduce leverage for PDVSA. All that would imply a higher recovery value.

What overseas assets could investors try to seize?

PDVSA has refineries, tankers and receivables. Of course, the value of the oil assets depends in part on the price of crude. In August last year, Barclays estimated the total at between $8 billion and $10 billion, but that was with oil fetching at least $50 a barrel.

The operating assets of Citgo Holding Inc., PDVSA’s U.S. refining subsidiary, are already pledged to creditors. The unit’s $1.5 billion bonds due in 2020 are secured by a 100 percent equity stake in Citgo Petroleum Corp.

How did things get this bad?

During his 14 years in office, former President Hugo Chavez nationalized companies and expanded the government’s role in the economy. By the time of his death in 2013, domestic industry had been crippled, leaving Venezuela almost entirely dependent on imports for consumer goods. Those imports were paid for with revenue from oil.

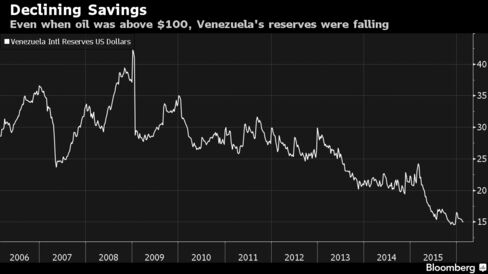

The economic model, characterized by government largess and inefficiency, was nonetheless more or less sustainable with oil prices above $100, despite the occasional shortage of toilet paperand the fact that the government had pledged much of its crude output to repay loans from China and in subsidies to regional allies such as Cuba.

As oil prices fell, the government relied more on creating new money to meet its expenses, helping fuel the fastest inflation in the world and making the black-market bolivar the worst-performing currency in the world.

By mid-2014, with oil hovering between $90 and $100, Venezuela was in trouble. President Nicolas Maduro, Chavez’s handpicked successor, could have boosted the country’s income in bolivars years ago by devaluing the official exchange rate of 6.3 per dollar at which it sold much of its hard currency. Yet he postponed the decision -- possibly out of concern for the inflationary impact such a move could have -- until earlier this month.

Now, with the country’s oil fetching about $25 a barrel, Venezuela’s crude income will fall toward $22 billion this year, according to Bank of America Corp. That’s barely enough to cover $10 billion of debt service on bonds, $4.3 billion of imports for the oil sector and $6.2 billion of payments on loans from China, the bank wrote in a note Feb. 8.

Even after reducing its gasoline subsidy and devaluing the currency, Venezuela won’t have enough dollar income left to pay debt and import food, according to economists at Barclays Plc and Nomura Holdings Inc.

Would a default be the biggest ever for a sovereign?

No, it would be the second-biggest. Greece defaulted on $261 billion in March 2012, according to Moody’s Investors Service data. Argentina defaulted on $95 billion in 2001.

Has Venezuela defaulted before?

Ten times on international debt, mostly in the 19th century, according to data from Harvard University economists Carmen Reinhart and Kenneth Rogoff. Venezuela first defaulted in 1826, 15 years after declaring independence from Spain.

Most recently, in 2005, it missed payments on bonds linked to oil prices after the government fired striking executives from PDVSA and the resulting chaos meant that the prices needed to calculate the payments weren’t available. The bonds it defaulted on were so-called Brady bonds, which were the result of a debt restructuring following a default in 1990.

How would a Venezuelan default differ from Argentina’s?

With any luck it won’t go on as long. Argentina’s default has dragged on for 14 years as the country battled investors who refused to accept losses of 70 cents on the dollar in U.S. courts. Venezuela, on the other hand, would probably be motivated to settle sooner in order to free up its oil shipments, according to Nomura.

Venezuela’s bonds have collective-action clauses, which mean that reaching a restructuring agreement with a majority of bondholders would require everyone to go along with the deal. PDVSA notes don’t have that rule. Investors are divided as to whether this makes default on one or the other more likely or easier to resolve.

“Each sovereign default is unique,” Siobhan Morden, the head of Latin American fixed-income strategy at Nomura, wrote in a note to clients in February.

Is there any hope that things can get better?

There’s a case to be made that not all is lost.

First, Maduro has announced cuts to subsidies on gasoline and a devaluation of the currency, which would allow it to stretch its dollar income much further. So far economists say the moves have been too timid to make any real difference, but they at least show that the government is concerned and is aware of what needs to be done.

Second, the political opposition is gaining ground. The opposition won two-thirds of the National Assembly in elections late last year, giving it widespread powers to dismiss ministers, block presidential decrees and block court appointments.

Third, China could appear with new financing. The Asian nation has already lent it about $17 billion and could presumably come to the rescue again.

Fourth, oil prices could rise. The country can scrape by with an average price this year of $50 to $65 a barrel, according to estimates from Barclays, Bank of America and Nomura.

Bank of America Corp. says it expects Venezuela to make all of this year’s bond payments, because it has enough assets available to sell and clearly wants to pay.

Keine Kommentare:

Kommentar veröffentlichen