Very little about the Argentina situation is at all clear, but this is reasonably clear: Argentina won't default on its bonds today. Not because everything will magically get wrapped up by 5 o'clock, but just because Argentina's $539 million interest payment due today is subject to a 30-day grace period, so it's really due 30 days from today.

The story, remember, is: Argentina has some exchange bonds, which it wants to pay, and some holdout bonds, which it doesn't. Judge Thomas Griesa, of the U.S. District Court for the Southern District of New York, has ordered it not to pay the exchange bondholders unless it also pays the holdout bondholders, led by Elliott Management.1

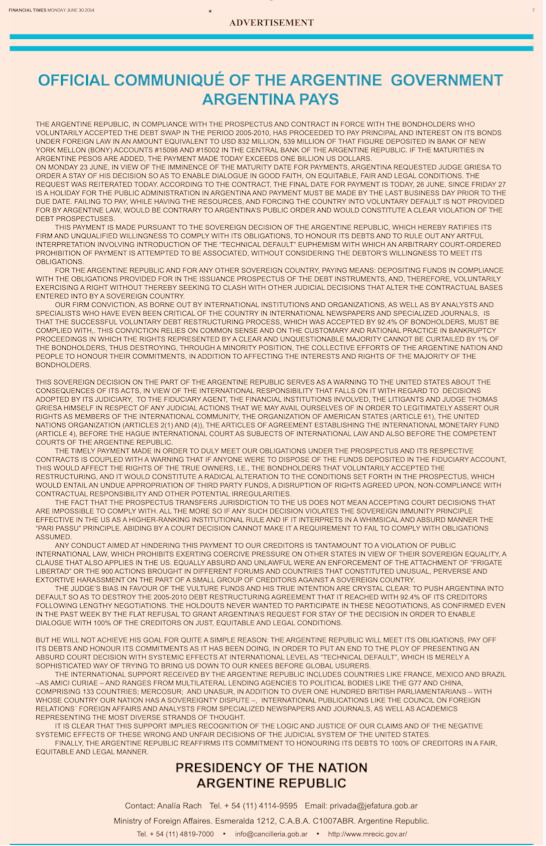

What can Argentina do in the next 30 days? One obvious answer is to negotiate a quick settlement with the holdouts. Two weeks ago I assumed that that's what would happen, since both sides have really good reason (1) to want a deal and (2) to want a deal before Argentina defaults. Since then, though, you would not say the rhetoric has been particularly friendly? Here is a furious, all-caps "Official Communiqué of the Argentine Government," published today, denouncing the "judge's bias in favour of the vulture funds." A friendly settlement does not exactly feel imminent, though again, they've got a month, and they do seem to like dramatic brinksmanship.

{kind=link}

But what are the other options, besides negotiated settlement and catastrophic default? Below I've collected some schemes that I find interesting, which are very different from schemes that I think would work. These are just ideas that tickled my fancy, and that I pass along to you in case you are similarly ticklish.

Scheme 1: Default, then settle using CDS money.

This scheme looks a lot like settling before the 30-day grace period expires, except that it takes place just after the 30-day grace period expires. Argentina misses the grace period, defaults on its exchange bonds, then cures that default by paying interest the next day. And the day after that, it announces a settlement with Elliott and friends.

What is the appeal of this plan? Well, as I've noted before, it is widely (though not universally) assumed that Elliott owns a lot of credit default swap protection on Argentina's bonds. If Argentina defaults, that will trigger that CDS, and Elliott will be in line for a big payout. If that payout is, say, $500 million, then Elliott should be indifferent between receiving, say, $2 billion worth from Argentina or $1.5 billion from Argentina and $500 million from its CDS contracts.2

In other words, this is the trick that Blackstone used with Codere: Do a quick default on your bonds so that your creditors get paid on their credit default swaps, and have them apply the money they got from their CDS to get you more favorable terms. I was fond of this trick when Blackstone used it, and I'd be at least as fond of it if Argentina did the same.

One problem with this scheme is that it is not entirely clear how much CDS Elliott owns, and so how much value can be extracted there. Also, any settlement probably involves giving Elliott new bonds, and a default does nothing good for the value of those bonds. If Argentina defaults again -- particularly as part of a scheme with Elliott -- that is not, you know, great for its reputation in the international bond markets.3

The other potential problem is: This requires actually paying Elliott. I don't know if this is a problem! Giving Elliott some money is sort of a necessary part of settling this dispute. But if Argentina really is prepared to go to the ends of the earth to prevent Elliott from seeing a dime -- as its rhetoric sometimes suggests -- then this trick won't appeal very much.

Scheme 2: Nondefault default.

This scheme involves Argentina sending money to its paying agent, and then saying, "what? We paid, it's not our fault if the U.S. payment system didn't get the money to the holders." Adam Levitin suggested this scheme on Credit Slips, and it seems to be a big part of Argentina's current plan. In defiance of Judge Griesa's orders, Argentina deposited the interest money with Bank of New York Mellon, the paying agent for the bonds. (Judge Griesa told BNY Mellon to send the money back.) That Official Communiqué is titled "Argentina Pays," and Joseph Cotterill interprets it to mean that Argentina is "prepared to argue that any payment it tries to make is enough to fulfil its obligations to the restructured bondholders: if the payment doesn’t go through, it’s the system’s fault."

This is not so much a scheme as it is just saying some magic words. One problem here is that those magic words may not be effective to avoid default under the terms of the bonds.4 But the bigger problem is that the magic words don't get money to holders, and eventually they will want their money. If your goal is to maintain access to the international capital markets, a technical argument that you've paid your debts isn't nearly as good as actually getting money to your creditors.

Scheme 3: Pay by check.

OK, now we're getting into the creepy stuff. This scheme starts with the fact that the investors who own Argentina's exchange bonds don't own any bonds. Instead, all the bonds are owned by nominees for clearing systems such as the Depository Trust Company (in the U.S.) and Euroclear and Clearstream (in Europe) on behalf of the investors, who own only claims on those clearing systems.5 This is true of basically all stocks, bonds, etc., and is normally very convenient: If you want to transfer a bond, you don't have to messenger over a very valuable piece of paper. You just have DTC make a few entries in your electronic account. The "global note" stays at DTC and never changes hands.

So the way payment normally works is, Argentina wires money to its paying agent, Bank of New York Mellon6 ; BNY Mellon wires the money to DTC as global noteholder; and DTC wires the money to its participants. (The participants tend to be brokers, so they're wiring the money on to their investor clients.)

The problem in this chain is around BNY Mellon: Judge Griesa won't let BNY Mellon send the money on to DTC, so it can never get to the holders. (The economic holders, that is: The DTC participants and their customers, not the technical global note holders.) On the other hand, if Argentina just put $100 bills in envelopes and mailed them to the economic holders, it's hard to see how Judge Griesa could stop it. Even if Argentina sent the bondholders checks, or even wire transfers, it could probably get away with that, since Judge Griesa's injunction doesn't apply to pure intermediary banks.

But Argentina doesn't know who the holders are: The only official holders of the bonds are the nominees of DTC and Euroclear/Clearstream. With corporate bonds, there'd be a solution: The holders could cut out the middleman by going to DTC and asking for a "certificated note" -- that is, for DTC to take your bonds out of its pool and give you an actual physical piece of paper representing your own bond. Then once you have your own bond, just, like, ask Argentina to send you a check.

Now, this doesn't seem to work for Argentina: Its bonds can only be held in global note form, unless Argentina decides to issue certificated notes.7 Can it just decide to do that? It ... seems unlikely. It would clearly be a violation of the injunction by Argentina,8 though Argentina doesn't care about that. But the injunction also applies to Argentina's agents, including BNY Mellon and DTC, and it would probably violate the court order for them to participate in any exchange like this.

The other problem here is that holding certificated notes is a big pain for the holders: They're harder to trade, to repo, to finance, everything. So if your goal is not to hose the exchange bondholders, making them hold certificated notes, even if you could do it, doesn't seem great.

Scheme 4: Forced wire transfers.

Here's one further layer of creepy, suggested to me by an emerging markets fund manager. This gets into the details of how Argentina has sent the interest payment to BNY Mellon. Here's what Argentina says(though it says it in all caps):

The Argentine Republic ... has proceeded to pay principal and interest on its bonds under foreign law in an amount equivalent to USD 832 million, 539 million of that figure deposited in Bank of New York Mellon (BONY) accounts #15098 and #15002 in the Central Bank of the Argentine Republic.

Who has that money? Well, what do you mean by "has," and what do you mean by "money"? Argentina "paid" that money by telling its central bank to electronically credit some dollars to BNY Mellon's account at the central bank. And BNY Mellon, in violation of the indenture but in accordance with a New York court order, didn't send the money on to the exchange bondholders.

What if Argentina ordered it to do so? Well, it probably wouldn't resist Judge Griesa's order. But what if Argentina "ordered" it to do so by making Argentina's own central bank move that electronic credit from the BNY Mellon account to another account -- say, the accounts (at the Argentine central bank or elsewhere) of the nominees for DTC, Euroclear and Clearstream?9 After all, it's all just electronic transfers, and right now those transfers are in the hands of Argentina's central bank. If BNY Mellon is defying its obligations to Argentina, why can't Argentina's central bank correct that?

That might be a little lawless, and I don't know whether it could be done under Argentine law. But if it could, Argentina could have a little bit of fun by getting the money even one step further down the chain -- not to BNY Mellon but to DTC, Euroclear and Clearstream.

Now, it's perhaps only a little bit of fun: Judge Griesa's order forbids the clearinghouses from passing on payments to exchange bondholders, so the money might be just as stuck at DTC and Euroclear and Clearstream as it currently is at BNY Mellon. But maybe not.

In particular, the holders of euro-denominated exchange bonds think that Judge Griesa's order should not apply to Euroclear and Clearstream. Here's the motion they filed on that subject yesterday, and -- though I am no expert -- it seems pretty compelling. In particular, the euro exchange bondholders argue that the payment process for the euro bonds occurs entirely outside of the U.S., that Euroclear and Clearstream are not subject to U.S. jurisdiction, and that Belgium and Luxembourg -- where Euroclear and Clearstream, respectively, are located -- forbid those clearinghouses from holding up payments because of a U.S. court order.

So if Argentina can get the money to Euroclear and Clearstream, there's a decent chance it can pay off its euro bondholders, at least: Either Judge Griesa will just release Euroclear and Clearstream from the order, or else a European court will order them to ignore the order and they'll do so.10

Getting the money to DTC doesn't do as much for the holders of the (larger) U.S. dollar exchange bonds, but it does something. For one thing, if DTC has their money and doesn't give it to them, the bondholders can sue it. So far this has been a hypothetical, as the money has never gotten that far, but if it does -- if DTC is holding money solely as a clearinghouse for the exchange bondholders -- then they have a case that it should give it to them. (And that DTC is not an agent of Argentina but rather just holding on to bondholders' property.) It's worth a shot: Judge Griesa will not sympathize, but perhaps an appeals court would.

That's particularly true if the euro-denominated bonds are getting paid while the U.S. dollar ones aren't. Today is a bit of a rough day for the U.S. dollar as the global currency. BNP Paribas is being severely punished for violating U.S. law outside of the U.S., because it used dollars, and "Pretty much any dollar transaction -- even between two non-US entities -- will go through New York City at some point, where it comes under the jurisdiction of US authorities." It's enough to make you not want to use dollars for your international transactions.

And so in fact here is a Wall Street Journal article about how Russian companies have come back to international capital markets using euros, not dollars, because "U.S. banks are still cautious about dealing with Russian borrowers amid the tensions with Ukraine and the lingering possibility of further sanctions." The more useful the dollar is as an instrument of U.S. foreign policy, the less useful it is as a currency for global transactions.

More generally, if you prevent one or two pariahs from using dollars, then you can cut them off from the global financial system. But if you prevent enough pariahs from using dollars, then you eventually cut the dollar off from the global financial system. We're a long way from that, obviously. All the same, you can see the problem if Argentina's euro bondholders get paid normally while its dollar bondholders are caught up in never-ending drama. A quick settlement here would be good for Argentina, and probably at least as good for Elliott. But it would be good for America too.

1 For more, see footnote 2 here. The Elliott entity involved is technically NML Capital, and Aurelius Capital is also a holdout plaintiff, but I just call the plaintiffs Elliott for my own convenience.

2 Actually Argentina would probably give it bonds, not cash, so it might prefer $1 of cash to $1 of present value of Argentine bonds.

3 Also of course the default could trigger acceleration by the exchange bondholders, and make Argentina's problem even worse, though I think if you did it quick enough you could probably avoid that. See in particular section 4.2 of the indenture, which allows for cure of defaults before acceleration.

5 There are limitless levels of detail here. Technically the bonds are not owned by DTC and Euroclear/Clearstream, but by "nominees" for those clearing systems. (See page S-19 of the prospectus.) DTC's nominee is Cede & Co., while Euroclear's and Clearstream's is Bank of New York Depositary (Limited) in London. (See this declaration by a Bank of New York officer, as well as Judge Griesa's 2012 opinion("There are two registered owners for the 2005 and 2010 Exchange Bonds. One is Cede & Co. and the other is the Bank of New York Depositary.").

6 Technically: "The Republic transfers funds to a US Dollar deposit account in the name of the Trustee at Banco Central." The "Trustee" is Bank of New York Mellon as indenture trustee; "Banco Central" is the Banco Central de la Republica de Argentina, Argentina's central bank.

7 See pages S-73 and S-74 of the prospectus.

8 From the injunction:

The Republic is permanently PROHIBITED from taking action to evade the directives of this ORDER, render it ineffective, or to take any steps to diminish the Court’s ability to supervise compliance with the ORDER, including, but not limited to, altering or amending the processes or specific transfer mechanisms by which it makes payments on the Exchange Bonds, without obtaining prior approval by the Court;

9 Confoundingly, a BNY Mellon entity -- though a U.K. one -- is the Euroclear and Clearstream nominee. See footnote 5.

10 The euro bondholders also want the judge to excuse BNY's Luxembourg branch, the paying agent on the euro bonds, from the order; that one seems harder. But if it works then Argentina can pay the euro bondholders without any shenanigans.

To contact the writer of this article: Matt Levine at mlevine51@bloomberg.net.

To contact the editor responsible for this article: Tobin Harshaw at tharshaw@bloomberg.net.

Keine Kommentare:

Kommentar veröffentlichen