And yet somehow — we sense the pari passu saga isn’t over yet.

This would be despite the completeness of Argentina’s defeat in the sovereign debt trial of the century…

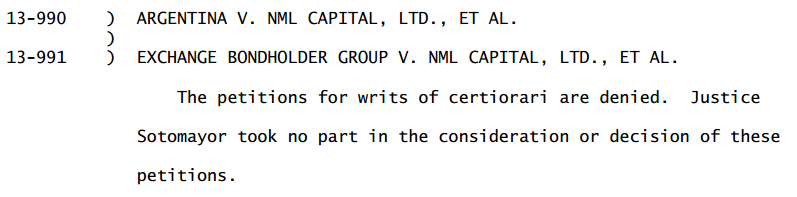

After all, the Supreme Court didn’t even ask the Solicitor-General about the US government’s views before rejecting the petition from Argentina (a process which could have taken months).

That suggests the court wasn’t worried by Argentina’s argument that sheer scope of the injunction on it to pay holdouts — alongside restructured bondholders, as a remedy for violating the pari passu clause in its defaulted debt — threatened core US legislation on sovereign immunity. That argument was Argentina’s best shot at getting the pari passu case overturned, and in particular, preventing holdouts from intercepting payments sent to other bondholders in New York.

In fact, on Monday Argentina also failed to win its other Supreme Court case on sovereign immunity grounds. Ruling seven to one, the justices decided that the holdouts are allowed to “seek information about Argentina’s worldwide assets generally” to enforce judgment debt.

Argentina’s loss of this discovery case also marks another expansion for creditor rights following sovereign default. Only Justice Ginsburg was left to dissent against the US legal system becoming a a “clearinghouse for information” on sovereign assets.

Which brings us to the other legal landmark in Monday’s decision — before considering options, if any, left to Argentina now.

Pari passu forever

Pari passu will now be enshrined as a powerful enforcement device in New York-law sovereign debt. Without Supreme Court review, the case law created by firstly the District Court for the Southern District of New York, then the Second Circuit Court of Appeals will stand.

This law supports courts in deciding that ratable payment could be a remedy to use against sovereigns who refuse to pay their debts, and that third parties — settlement banks, clearing systems, other bondholders — may be sued if they are seen to handle funds in violation of such orders.

To a great extent, other sovereign debtors to whom this case law might be applied in future have Argentina’s recalcitrance to thank for this outcome. If the Republic had settled with holdouts earlier — in place of fighting them in the courts, then stonewalling courts when the fight turned against them — the courts might not have developed such a punitive remedy.

The courts have throughout insisted that Argentina’s recalcitrance will isolate it as a precedent for pari passu litigation elsewhere: few other governments are as deadbeat and as badly-behaved as Argentina.

Even so that would hardly reassure third parties in the case who feel they are being used as instruments in someone else’s conflict. Other litigation against sovereigns may be needed to decide where ‘recalcitrance’ starts and the usual harsh bargaining of debt restructuring begins. It may be unlikely that anyone is found to be as naughty as Argentina has been in treating creditors equally (it passed laws to subordinate holdouts), and sovereigns don’t restructure debt very often.

Still, with the Supreme Court putting a lid on the case, future sovereign bond holdouts will be able to bank some useful law. This is along with the probability that Argentina will have to settle with NML at some point, to make the pari passu threat ultimately go away. That means NML gets paid much more than previous restructuring terms, even if not fully.

Pay, default, settle

We think the only ultimate answer is for Argentina to settle, whenever it thinks it has the best negotiating leverage. Losing at the Supreme Court would cut a lot of that leverage away.

Still:

– The next restructured bond payment (ie, the first time the holdouts could seek to enforce the order) falls on June 30.

– Over that period, Argentina has the right any time in the next 25 days to ask the Supreme Court to rehear its petition, under court rules. Rehearing requests never get through. But it’s more time on the clock if Argentina wants to avoid short-term consequences of courts lifting a stay on the order to pay.

– Argentina would need time to talk to its payment intermediaries about what to do. Those intermediaries themselves — Bank of New York, notably — need to analyse their obligations now as well.

– The restructured bondholders in particular may still have legal options. Holders of the English-law, euro-denominated restructured debt have already filed suit in Belgium to force Argentina to pay them there, as they have long argued that US courts do not have jurisdiction over their bonds. That case may revive. It could be a mess, as a Mexican standoff may thereby be created between two legal systems.

– Last but not least, the victorious holdouts will be watching Argentina like a hawk in case it prepares to reroute bond payments outside New York. Which we’d guess would take time to set up — given how Argentina’s lawyers described the options…

– Yet the one the market will be attempting to digest — Argentina’s benchmark restructured bonds had dropped about ten points in price at pixel time — is whether the Republic defaults on everybody.

The incentive to do this would be to restore some of that lost leverage, we suppose. But that seems unlikely if holdouts have won such an early legal victory — they can resist any future restructuring on the same basis of unequal treatment (pari passu). And after all, defaulted restructured bondholders would surely look at legal options too.

Default does seem likely if Argentina stays clueless about what to do here — but Monday’s loss still makes a settlement seem the only way out here.

Keine Kommentare:

Kommentar veröffentlichen