The negative zone

Not that negative zone – Europe:

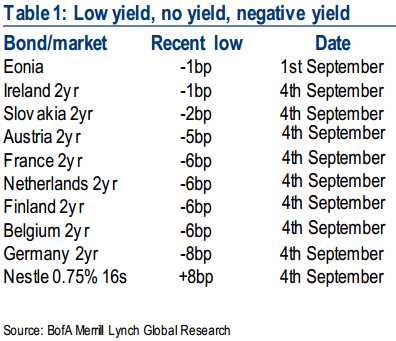

Already, close to 60% of our European government bond index yields less than 1%. That’s €2.6tr of government bonds in Europe returning virtually nothing for holders. Quality yield is proving elusive for investors…The problem of low yields is rapidly becoming a problem of no yield in some parts of the market. Yesterday’s surprise ECB rate decision lowered the deposit rate further into negative territory, from -10bp to -20bp. Front-end government bonds saw their yields fall sharply on the back of this. As Table 1 shows, eight European government bond markets now have 2yr yields in negative territory. In credit land, the prize goes to the Nestle 2016 bond, where its yield is now a paltry 8bp.

That’s from Bank of America Merrill Lynch’s European Credit Strategist note on Friday.

No surprise then that bond-buyers are increasingly chasing European corporate credit instead, as BAML point out. Relative to government paper, corporate bonds offer two to three times the yield at this point.

But then the absolute yield is still barely 1 per cent, for quality credits (like Nestle).

What’s being said by equities at the same time? There are only 11 stocks in Europe which could be called big (market caps of over €5bn), and cheap (less than 10 times price to earnings, and below book value) with positive earnings momentum, according to Citi.

Nine of them are financials (the exceptions are Repsol and Renault), which you might expect to be pricing in the benefits of ECB action at this point.

For everything else the ECB’s action might have a rather more mixed message – that growth really is in trouble if the central bank needs to launch QE for the first time, and thus, the earnings outlook across the eurozone can’t be good.

On the other hand, the ECB buying not only ABS but RMBS is a huge signal to risk assets (and, we think, will make a big difference to capital constraints on lending). The negative zone’s about to get weirder.

Keine Kommentare:

Kommentar veröffentlichen