They did it! They finally did it, post-Second Circuit fiasco:

[Bloomberg] Argentina will send a bill to Congress tomorrow [August 27] to reopen a debt restructuring for those creditors who haven’t accepted previous swaps after the nation’s 2001 default, said President Cristina Fernandez de Kirchner…She also said that holders of restructured bonds, who accepted discounts of as much as 70 percent, will be able to swap them into securities governed by Argentine law in a bid to prevent payment disruptions from a U.S. court ruling in favor of the holdouts.

We first looked at the why and how of using a local-law swap to get round the pari passu problem which Argentina has made for itself — back in November. That’s how interminable this pari passu saga has been.

Much more in CFK’s speech. Come for the baldly disingenuous assertion that callingArgentina a “uniquely recalcitrant” debtor is “un poco injusto”; stay for confirmation that the new bonds would be paid through Caja de Valores, the local clearing house. Surely it’s not about showing credibility to the Supreme Court by reopening the swap to holdouts: the actual plaintiffs won’t take the offer, and the judges haven’t considered Argentina’s petition directly yet.

FT Alphaville’s considered take on all this? It’s pretty nuts.

We’re not alone in this of course, and in truth there’s not much to add. Is it actually crazy? Well, why announce the swap now? That’s our question. It covers three areas, and it’s at least interesting to consider how complex the saga is getting…

1.) It doesn’t imply much confidence on Argentina’s part that the current stay of the rulings can hold throughout the remaining appeals and Supreme Court process.

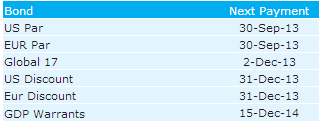

Via Barclays — those are the next payments on the (foreign-law) restructured debt. The late 2013 ones would be covered by the stay certainly so long as the Supreme Court considers the petition (and likely gives the US government months to provide its view). This is still a courtesy from the Second Circuit to the higher court, but it’s generous to Argentina in the circumstances. But it’s still roulette: you need the stay to be in place for each of those payments (and the next payments after those), even if there are months and months between each event in the Supreme Court litigation.

It’s worth bearing in mind that the current stay dates back to November last year. Itsterms said that Judge Griesa’s “November 21, 2012 orders… are all stayed” with respect to enforcing the injunction. As of the August ruling, “the amended injunctions shall be stayed” pending Supreme Court review of a “timely” cert petition by Argentina. “Timely” might not even mean the cert petition which has already been filed, implying a longish period of time. More on this below.

It’s possible, as Mark Weidemaier notes, that “all stayed” covers Griesa’s order for Argentina not to try “altering or amending the processes or specific transfer mechanisms by which it makes payments on the Exchange Bonds”. (Where a local-law swap surely fits the bill.) We’d assumed before that this bit wasn’t stayed, but we’d be the last to underrate the importance of loopholes in this case.

In any event there’s one cynical way to look at this. If Argentina could quite legally offer a swap during the stay, why not do it sooner — now — rather than later?

Well, a better question: would it really be a good idea to tempt fate here?

It’s an invitation to the holdouts to demand the stay is lifted given Argentina’s continued defiance. They’d surely do this anyway the next time an Argentine government official said something about not giving the vultures a red cent, but this is an enticing loophole.

More to the point, the Second Circuit has just made clear it doesn’t like ways of dealing with holdouts that “ignored the outstanding bonds and proposed an entirely new set of substitute bonds”. The gist of CFK’s plan also seems to involve suspending the lock law which US courts have seen as such an overt tool of subordination. Not abolishing it.

Giving an ear to the holdouts, the courts might say the stay didn’t mean to allow a swap in the first place, or they might have the terms amended anyway. In any case, Argentina’s own hedging against removal of the stay might risk lifting the stay. Not so much roulette as self-fulfilling prophecy.

2.) Nor does it imply Argentina had much confidence that Supreme Court litigation can transform this case, or buy enough time to come up with the next cunning plan.

That’s actually… fairly rational of Argentina, if it did think that. Fairly. The substance of its first petition to the Supreme Court wasn’t spectacular: Argentina didn’t have the final ruling on actual payments to complain about yet, so it was limited to alleging abuses of sovereign immunity and equitable relief by federal courts. (It hammed it up by claiming this was all “unprecedented” — it could well be — but that might be a red flag to the Supreme Court for taking up the case.)

This still doesn’t explain why Argentina is launching the swap now. That’s because the Supreme Court’s basic value to it is surely still the time on the clock it brings. Barclays analysts on Friday argued that SCOTUS end-dates for Argentina might lie as far out as June 2014 (if judges took the case on to next term’s docket and it went to argument, after granting cert) or June 2015 (if this term’s docket was full before granting cert). Any 2015 date is interesting because it heads into the point where restructured holders couldn’t sue Argentina for offering better terms than they got to holdouts, in any future deal.

This assumes the granting of cert. But then the Second Circuit’s ruling on Friday seemed to allow for a second petition by Argentina — maybe for it to complain about the payments aspects or treatment of third parties.

So with all that time on offer, it still seems weird to aggressively seek insurance on a defeat at the Supreme Court (particularly as the reported swap terms seem to imply some kind of trigger on a defeat there). What else then?

3.) The August 23 ruling might have made clear that the institutions necessary for payment of the restructured debt (which is a list starting with Bank of New York) can’t be relied on the next time Argentina tries to make a payment.

This is one of the more interesting ways to look at the swap. On the whole, Friday’s Second Circuit decision came down like a ton of bricks on third parties trying to get themselves carved out of the injunction itself.

The intriguing thing is what would happen to BNY, the trustee for the bonds, or a clearing house, should they still be in the frame when a restructured payment comes down the tubes without any accompanying payment to holdouts.

It’s nothing good — the court suggested that financial third parties “are already called on to navigate US laws forbidding participation in various international transactions”: putting the wrong kind of payment on restructured sovereign debt in the same box as money-laundering controls. But it still read unclear to us if it would be automatic contempt to assist Argentina. All the Second Circuit said was that BNY etc “will be entitled to notice and the right to be heard” if someone sued over this stuff.

But that’s kind of belied by Judge Barrington Parker more or less using a great big foam-finger to point to “exculpatory clauses” in BNY’s trustee document that the bank could use to avoid a suit. (Footnote 11 of the judgment). Which is why it’s hard to see the bank not using these clauses to get out now, or in advance of a contentious restructured payment.

In which case Argentina’s race to get Caja de Valores on board makes more sense. But then the moves to create a new payment structure might anger the US courts enough to scare away the existing structure. Not easy to arrange a bond swap on your own.

And so to see if the stay holds…

Keine Kommentare:

Kommentar veröffentlichen